Our flexible approach could help buy your first home

You’ve saved your deposit, found a property and are ready to make yourself at home. It’s a big commitment with a lot of change. The good news is we’re here to help try and make the move to home ownership that bit easier.

We won’t hold that unpaid phone bill against you before you start climbing the property ladder. Our flexible approach to credit assessment means we’ll consider small credit issues when we assess your application. It's just one of the ways we see the real you when the big banks might just see numbers. Talk to us about your situation and if we can find a way to help, we will.

Why Pepper Money?

We're fast: Credit decision within 1 working day

We're flexible: We'll always try to give you options

We're accessible: Talk through your situation with us

- Gifted deposits accepted

- Floating or fixed interest rates

- 60 day loan approval

- We look beyond just your credit score

- Get a quick response within 1 working day

- Borrow up to 85%* of the property value

What credit score do I need to buy a home?

We don’t just look at the black and white boxes on your application. We make the effort to get to know the person behind the application and understand your personal circumstances.

We ask the questions that matter and uncover the reasons behind any small credit issues on your credit report. This allows us to assess your application in-line with our responsible lending obligations and make an informed decision on your ability to repay your loan. What this means, is you could still apply for a Pepper Money home loan even with a less-than-perfect credit history.

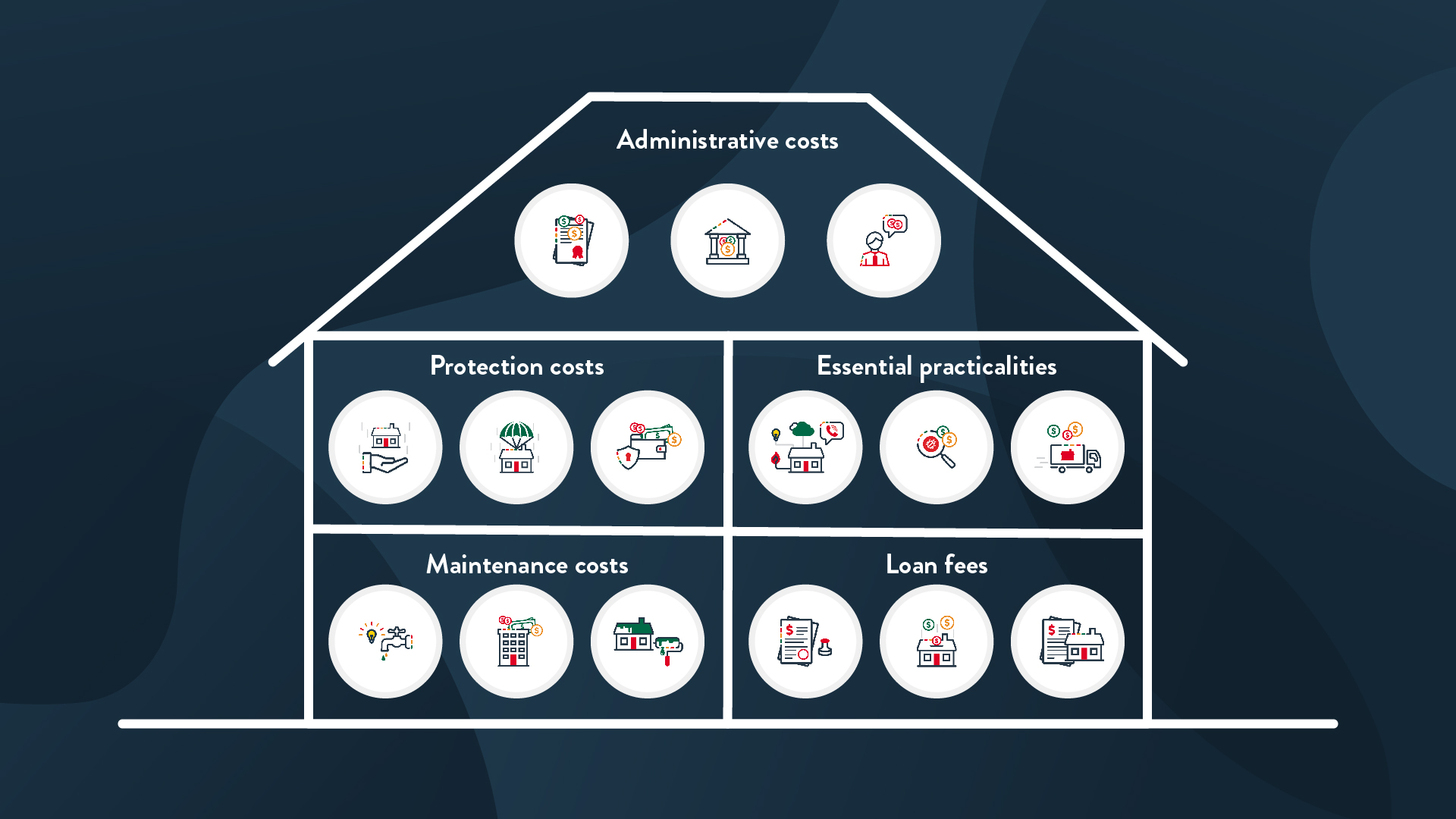

How much deposit do I need to buy my first property?

Saving your deposit is often the hardest part of buying your first property. But the good news is that may be able to help after you've saved your 20% deposit. You’ll also need some funds in reserve for conveyancing and legal fees – and don’t forget about any new furniture or decor you'll want to buy!

We may also be able to help if you’ve recently been gifted all or part of your deposit; for example, if it's through inheritance, or a very generous family member.

Any loan applications are subject to the Pepper Money team completing responsible lending checks and considering your/every customers individual circumstances.

Your Loan, Your Rate

Discover our flexible approach to home loans. We look at a range of factors (including your financial situation, credit history and property) to provide eligible borrowers with an interest rate estimate. Talk to a lending specialist to find out where you stand.

Crunch the numbers with our calculators

Borrowing Power Calculator

Mortgage Repayments Calculator

Budget Planner Calculator

Savings & Deposit Calculator

Learn more about our first home buyer home loan

The choice is yours

20% deposit

Non-metro lending

-

Interest rates

-

Floating interest rates from 6.69% p.a. to 10.90% p.a.1

2-year fixed interest rates from 6.44% p.a. to 10.65% p.a.1

3-year fixed interest rates from 6.49% p.a. to 10.70% p.a.1

The actual interest rate will depend on the borrower's circumstances and the information verified during the assessment of a loan application.

-

Loan purpose

-

Purchase or refinance an owner-occupied or investment property. Debt consolidation available when refinancing.

-

Maximum LVR

-

Borrow up to 85%* of the property value.

-

Loan amounts

-

From $100,000 up to $2,500,000 subject to product, region, eligibility criteria and lending limits.

-

Loan terms

-

10 - 30 years - subject to eligibility criteria.

-

Interest rate options

-

Choose a floating rate or a 2 or 3-year fixed rate period.

-

Repayment options

-

- Principal and Interest, or

- Interest only (up to 5 years - followed by Principal and Interest payments for the remainder of the loan term).

For owner-occupied loans, interest only is limited to 50% of your total loan amount.

-

Repayment frequency

-

- Weekly, fortnightly or monthly for Principal and Interest loans

- Monthly for interest-only loans

-

Extra repayments

-

Unlimited extra payments are permitted, free of charge for floating interest rates. For fixed rate loans, extra payments are free of charge up to $10,000 p.a.

See fees and charges for more information. -

Redraw

-

Minimum online redraw is $50, and minimum manual redraw is $1,000.

You'll need at least 1 floating loan split to transact via redraw.

Redraw is not available during any fixed interest rate loan term. -

Loan splits

-

Up to 4 splits are available.

-

Fees and Charges

-

Establishment fee: $749 inclusive of legal and settlement fees.

Discharge admin fee: $500

Monthly admin fee: From $10-$15 per loan split, depending on product.

Break costs: Break costs are payable on early repayment of more than $10K p.a. on a fixed rate loan, or switching to a different interest rate during the fixed rate period.

A default interest rate, which is your current interest rate plus 2% p.a. may be charged on each amount that is either overdue or over the limit of your home loan.

Any loan applications are subject to the Pepper Money team completing responsible lending checks and considering your/every customers individual circumstances.

Need some help with your first home loan?

Whether you’re confused the purchase process, wondering what LMI or LVR mean, or are looking for help along the way, our resources are here to make sense of all that finance jargon.

Don't forget to read this bit...

Information and interest rates are correct as at 3 September 2024 and subject to change at any time. Offers and promotions may be continued, withdrawn, or changed at any time without notice.

*Offer applies to ‘New Build’ Prime, Near Prime and Specialist Full Doc home loan applications with LVR >80 - 85%. Available for Metro security locations only. A New Build is a property where the borrower has made a financial and legal commitment to buy in the form of a purchase contract with the builder, prior to the property being built or at an early stage in construction. This could be traditional ‘construction lending’ where the loan is disbursed in staged payments, or it could be a loan to finance the purchase of a property, which will be settled (in one payment) once the build is complete or a newly-built entire dwelling completed less than six months before the mortgage application. The dwelling must be purchased from the original developer (the contract to buy at completion can be agreed while the building is still being constructed).

1Carded floating and fixed interest rates range from 6.64 - 10.90%p.a., are correct as at 7 March 2025 and subject to change at any time. See the latest rate card for more information. The actual interest rate applicable will depend on the individual borrower’s circumstances. A default interest rate, which is your clients' current interest rate plus 2% p.a. may be charged on each amount that is either overdue or over the limit of their home loan.

Information provided is factual information only, and is not intended to imply any recommendation about any financial product(s) or constitute tax advice. If you require financial or tax advice you should consult a licenced financial or tax adviser.

All applications are subject to credit assessment, loan eligibility criteria and lending limits. Terms, conditions, fees and charges apply. The actual interest rate will depend on the borrower’s circumstances and the information verified during the loan application assessment.